How to afford law school without generational wealth

How to afford law school without generational wealth

A tuition discount here, a loan forgiveness program there, and you're on your way to freedom from $100,000s in debt

Welcome to my Substack, where I pass on my learnings navigating the legal profession as a first-gen law student at Cornell Law! You can always reach me at allisoninwonderland@substack.com.

I learned from my mother that you can haggle with anyone, even the Home Depot cashier for a discount on a curtain rod with a rip in the bag, though you should be prepared for (or perhaps hope for?) a face that screams “I just work here man.”

It was one of my proudest Second Generation moments. A 10% discount (2 bucks at most) is no windfall, but I had overcome my embarrassment of being someone who loves a good deal. It runs in my blood. And apparently in the blood of many Asian Americans, as comedian Jimmy O Yang so aptly recounts in this snippet of his standup routine:

There’ll be hot dog street vendors out there, right? Latino brothers selling bacon wrap hot dogs for $5? I love those things! And my dad will go up and haggle with them. He’ll go and be like: OK, I give you five dollahs for two hot dogs. I’m like, Dad, it’s not ‘buy one, get one free’ at Costco. Just give him $10.

He’s like “Shhh! Never pay full price.”

“OK, I give you $8 for two hot dog. Final offer.”

And the guy doesn’t care. He’s like “No, it’s $10.” And then my dad has his strategy, he just announces in front of everyone, makes sure everyone hears him…

“OK! We WALK AWAY.”

I’m like, Dad I don’t think he cares if you walk away. Don’t walk away, I’m hungry! He’s like:

“It’s better to be hungry than pay full price.”

Then my mom comes up behind us with four hot dogs, and she’s like, “Guess how much?”

Last post, we visualized what it looks like to pay off your loans. In this post, we look at whether it pays off to choose the cheaper school.

The process starts before haggling

Getting a good deal on law school starts way before you have acceptance in hand, to the tune of:

Before applying, boosting your “stats” — The higher ranked your undergraduate, GPA, and LSAT, the more likely you will (1) get into law school and (2) receive better merit aid.

Applying to a range of schools, including where you’re in the top quartile — Create options for yourself. The higher you stack compared to your peers, the more money you’ll get.

Negotiating — Always ask for money, need-based if possible and definitely merit. The worst that can happen is they say “no.”

Choosing your school with financial realism — To be discussed below.

Comparing loan burdens

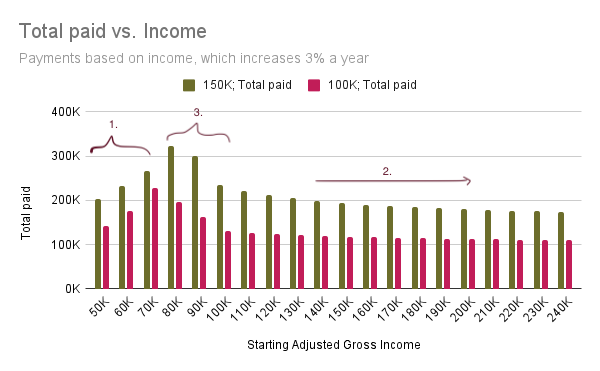

You’ll likely have a few options on the table after you finish the admissions cycle. Tuition-wise, I was left with the option of attending NYU for a total of $150,000 (which is the typical total loan burden) or Cornell for $100,000.

The graph below compares the amount I would have paid over a lifetime between the two schools.

If you have lower loans to begin with, you’ll pay less overall — obviously. But there are certain points where it is more “expensive” to have a $150,000 loan.

At the lowest incomes, you’ll need your loans forgiven no matter what. The tax on forgiveness ends up reflecting the original difference between $150,000 and $100,000 – $50,000.

But! If you’re in public interest, you could have your loans forgiven tax-free after 10 years with the Public Service Loan Forgiveness program (PSLF). Because it isn’t taxed, there is no difference between taking $100,000 versus $150,000 in loans.

At the higher incomes, you’re chipping away at the original loan so that interest doesn’t build up as fast. That’s why the difference in the amount paid is pretty much the original difference between $150,000 and $100,000 – $50,000.

The difference between $150,000 and $100,000 isn’t that big. You’re forking over disposable income and paying off your loans in 3-5 years.

It’s the middle incomes of $80,000 to $100,000 where the difference matters. You may pay $100,000 more overall on a $150,000 loan than a $100,000 loan – that’s two times the original difference.

Why? You can feasibly chip away at the interest and capital of a $100,000 loan. On the other hand, interest is larger on the $150,000 loan, so you’re not as aggressively chipping away at the original loan and interest continues to grow, causing the relative difference between the two loans to be greater than $50,000 after 10 to 20 years.

So should I always choose the less expensive school?

My Chinese heritage says yes, my official answer is that It Depends™. (Learn to sling these two words and you’ll be a bonafide lawyer in no time). These are the factors that should go into your decision.

What are my goals?

To build wealth? To enter the public service?

What kind of lifestyle do I want to live?

Where do I want to live?

What kind of jobs can I get after graduating from X school?

Do these jobs correspond to my lifestyle and location goals?

What percentage of students can access that job? Does ranking matter? How highly must I rank?

Does this school make sense given the amount it would cost?

Is going to this school necessary for my goals?

Do potential jobs coincide with the salary I need to make to pay off my loans?

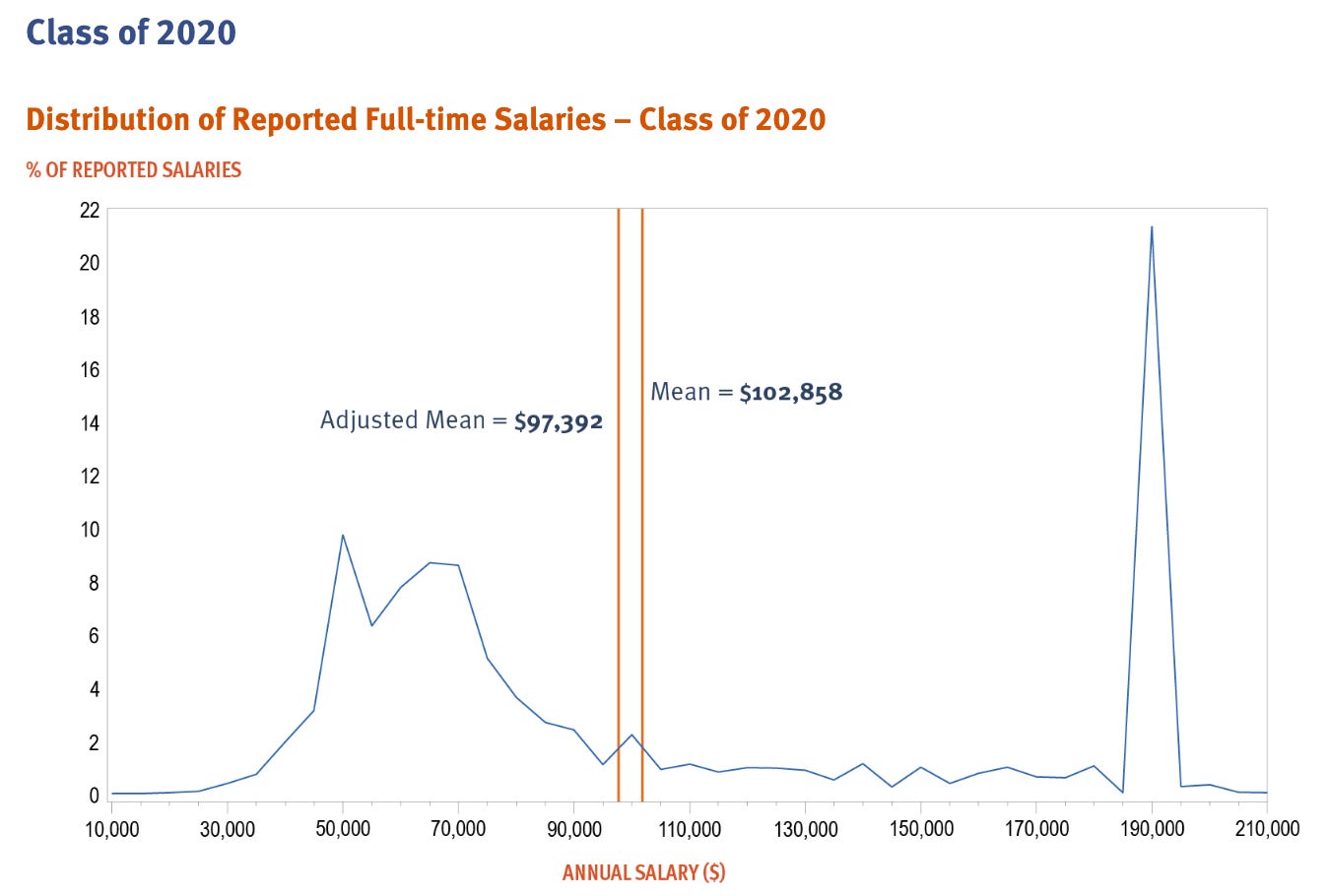

How much money do lawyers make?

Starting salaries cluster around $50,000 to $70,000 and $190,000. That low-range cluster on the left corresponds to public interest jobs, and that super-spike on the right corresponds to Big Law jobs. Then you have a minority of people who fall in the spaces in between.

As we found above and in the last post, because of accruing interest, it’s extra costly to pay off the typical $150,000 in loans when you make less than $100,000. People in public interest can benefit from the federal Public Service Loan Forgiveness program (reviewed below), but you might experience runaway interest in a private sector job that pays only about $100,000.

Yet that middle-income job might be the perfect fit for your goals. Unlike the $200,000 Big Law jobs that are clustered in certain cities, middle-income jobs are found everywhere. And work-life balance is reputedly much better.

If you were like me and didn’t know what any of these jobs entailed, here’s…

each job in a few words

Disclaimer: Outcomes vary.

Public interest — you’re the little guy in an understaffed firm making a bit more than minimum wage. Tuesday, you’re comforting a client catastrophizing because of a drug charge moments before you walk into the courtroom to defend them, and Wednesday, you’re sobbing in front of your computer while hammering away your legal argument. You probably aren’t worked around the clock, but that doesn’t mean you don’t toss and turn until 1am thinking about the moral ramifications of losing your death penalty case.

Big law — you’re making more than $200,000 straight out of law school with intensive oversight and training from successful lawyers, but you’re fated to “phubbing” as you answer emails around the clock. You might have a second wardrobe and a sleeping bag tucked into your office closet, and all your friends know that you tend to cancel plans last minute.

P.S., they say that Tax Law is the ideal Big Law area — it has the best work-life balance given a Big Law salary.

Mid-sized or plaintiff-side firm — you make around $100,000/year which might be barely enough to cover your $160,000 loan burden, but you live in Saratoga, FL to take care of your aging mother so what else would you spend it on, anyway? You get to go home to your husband at 6pm each weekday and can even hold weekend commitments without fear of canceling (take that, Big Law!).

My two cents on whether you should choose the less expensive school

Public interest track — you need’nt

If you are going into public interest, you’ll likely take advantage of the Public Service Loan Forgiveness (PSLF) program. The loan burden isn’t a problem so much as the general lack of disposable income. It will be difficult to create wealth.

If you’re trying to enter echelons of society accessible only to graduates from the T-5 schools, like the Supreme Court or certain policy positions, you may have to go to a T-5 school no matter the cost. Hopefully, you’ll be able to take advantage of PSLF.

Private sector track — usually, you should

I don’t recommend taking on more than $100,000 in debt from a law school if (a) that school doesn’t have pipelines to Big Law or (b) you don’t plan on working in Big Law. The math doesn’t add up.

Loan forgiveness for those in public interest

You may recall that there’s a teensy-eensy problem with making a low income… the fact that forgiven debt is taxed as income. For $150,000 in loans, you could pay as much as $100,000 in taxes in Year 20 when your loans are forgiven.

How could anyone choose to work in the public interest? Enter… the federal Public Service Loan Forgiveness program. The forgiveness of the PSLF program is tax-free.

I repeat: After 10 years of working full-time for qualifying public organizations, your loans are wiped away without it being reported as taxable income.

Here are some facts:

10 years need not be consecutive. To be exact, you need to make a total of 120 payments towards your loans while working with (a) qualifying employer(s)

Full-time means working 30 hours a week for one or more qualifying organizations (multiple employers allowed)

You must be a direct employee (not contractor) of the qualifying company (few exceptions apply)

Eligible employers include U.S.-based government organizations, 501(c)(3)s, and other not-for-profits – your employer qualifies based on the IRS Tax ID “EIN” (Employer Identification Number)

More about PSLF and other Q&A on the federal government website.

LRAP supplements PSLF

Law schools have “Loan Repayment Assistance Programs” that intertwine with the federal government’s loan repayment system. Your school makes loan payments for you, so you pay nothing out of pocket. This supports your ability to choose to work in public service.

Review the small font

Law schools tend to have two kinds of limitations on who can qualify for LRAP: Salary-based and need-based. The ole’ NYU versus Cornell comparison is instructive.

Cornell’s (pretty much) only stipulation is that you make less than $80,000/year. Above that, you pay off your loans. You can enter or drop out of the program whenever you want, just like you can enter or drop out of PSLF whenever you want.

NYU stipulates that you have total assets of less than $100,000 (reviewed each year) and that you make less than $110,000/year. But once you start the 10-year countdown, you can only leave the program for at most 2 years or else lose your LRAP eligibility altogether. This latticework of rules is balanced by the fact that you can choose the most aggressive federal repayment plan — a 10-year standard repayment plan — on which NYU pays. Your loan repayment behavior mimics what you would have been able to pay in Big Law, even though you’re in public interest. It’s an appealing safety net in case you leave public interest law.

Thanks for reading! If you didn’t catch my last posts, see:

How to ask for money once you have acceptance in hand

How federal loans work and how much you’ll pay back over time

And here’s a law school scholarship bank that might help you make law school more affordable.

Hmmm, I'm actually curious about your law school experience, so here I am! Excited to learn about a domain many of my friends have entered but which is quite opaque to me so far :)