What does it actually cost to go to law school?

What does it actually cost to go to law school?

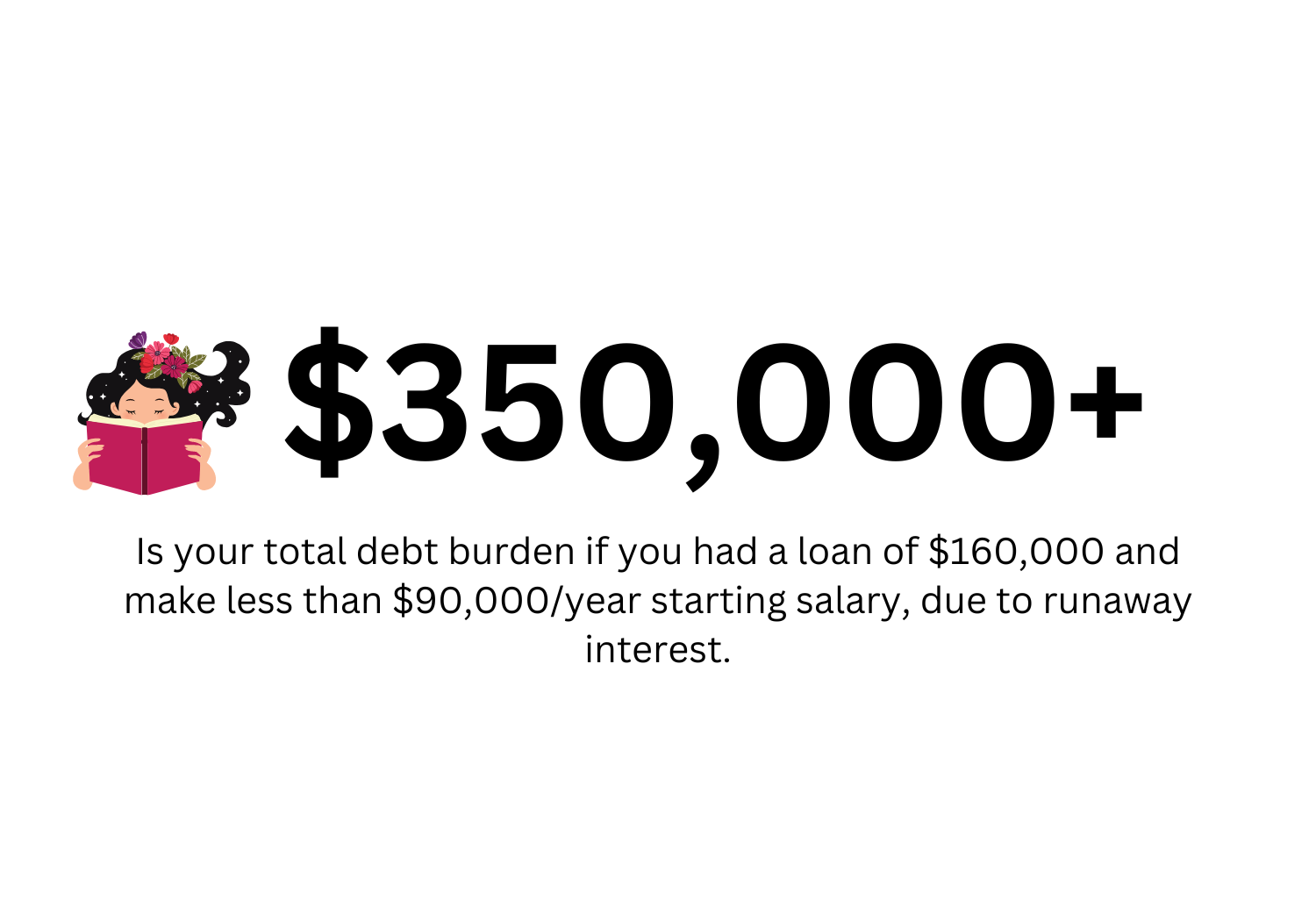

At a $100,000+ annual cost of attendance, will you be saddled to debt forever?

Welcome to my Substack, where I pass on my learnings navigating the legal profession as a first-gen law student! You can always reach me at allisoninwonderland@substack.com.

Are you daunted about going to law school because of the $100,000+ annual estimated cost of attendance? That was me! In the next few articles, I will try to break down financing law school so that you can make informed decisions about applying to and selecting your school.

Today, we review how much a typical federal student loan is, how repayment and interest work, and how much total you will likely fork over to the government.

How much debt are lawyers usually in?

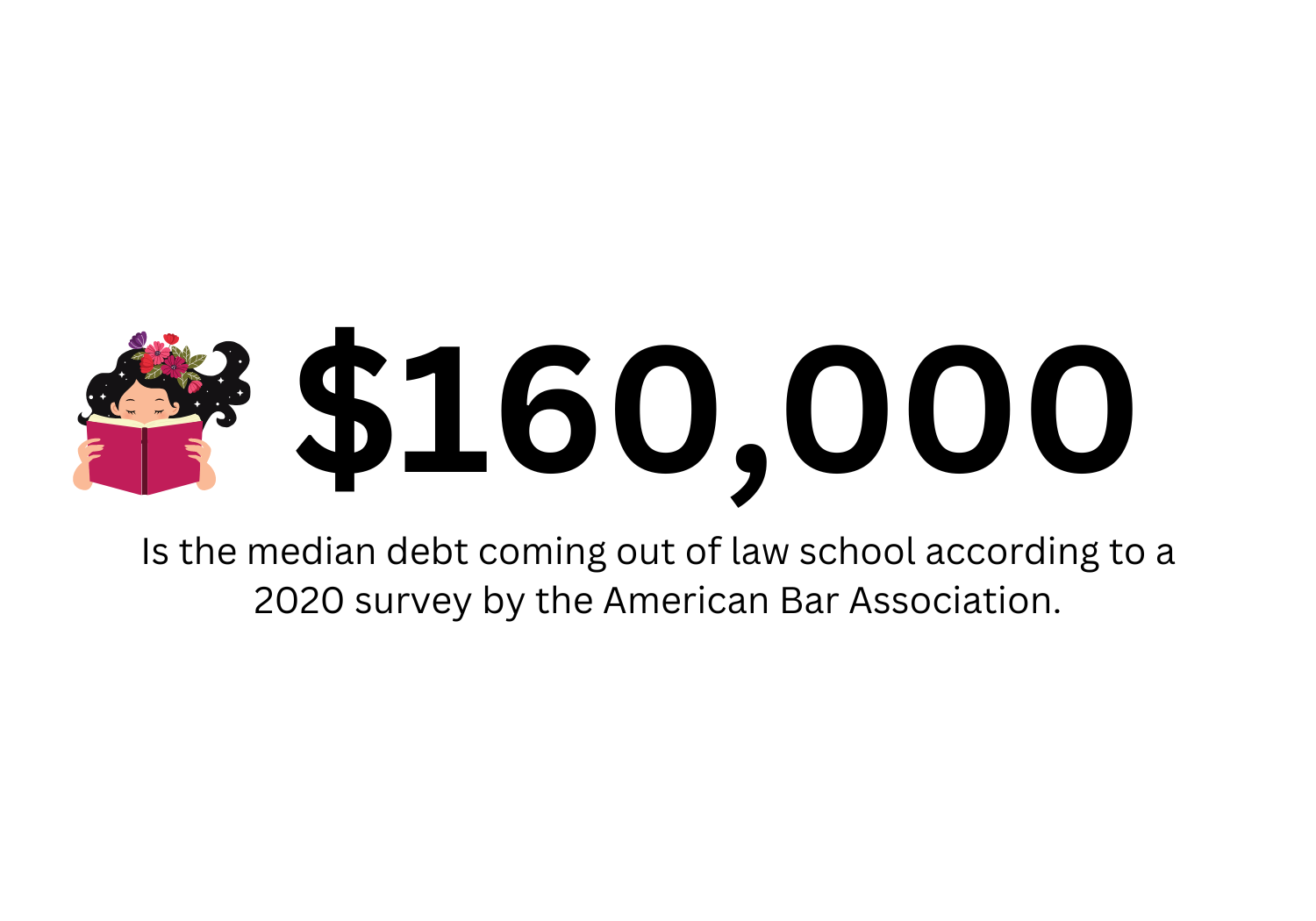

The median debt coming out of law school (including undergraduate debt averaging 28,000) is $160,000, according to a 2020 survey conducted by the American Bar Association (ABA) Young Lawyers Division and AccessLex Institute.

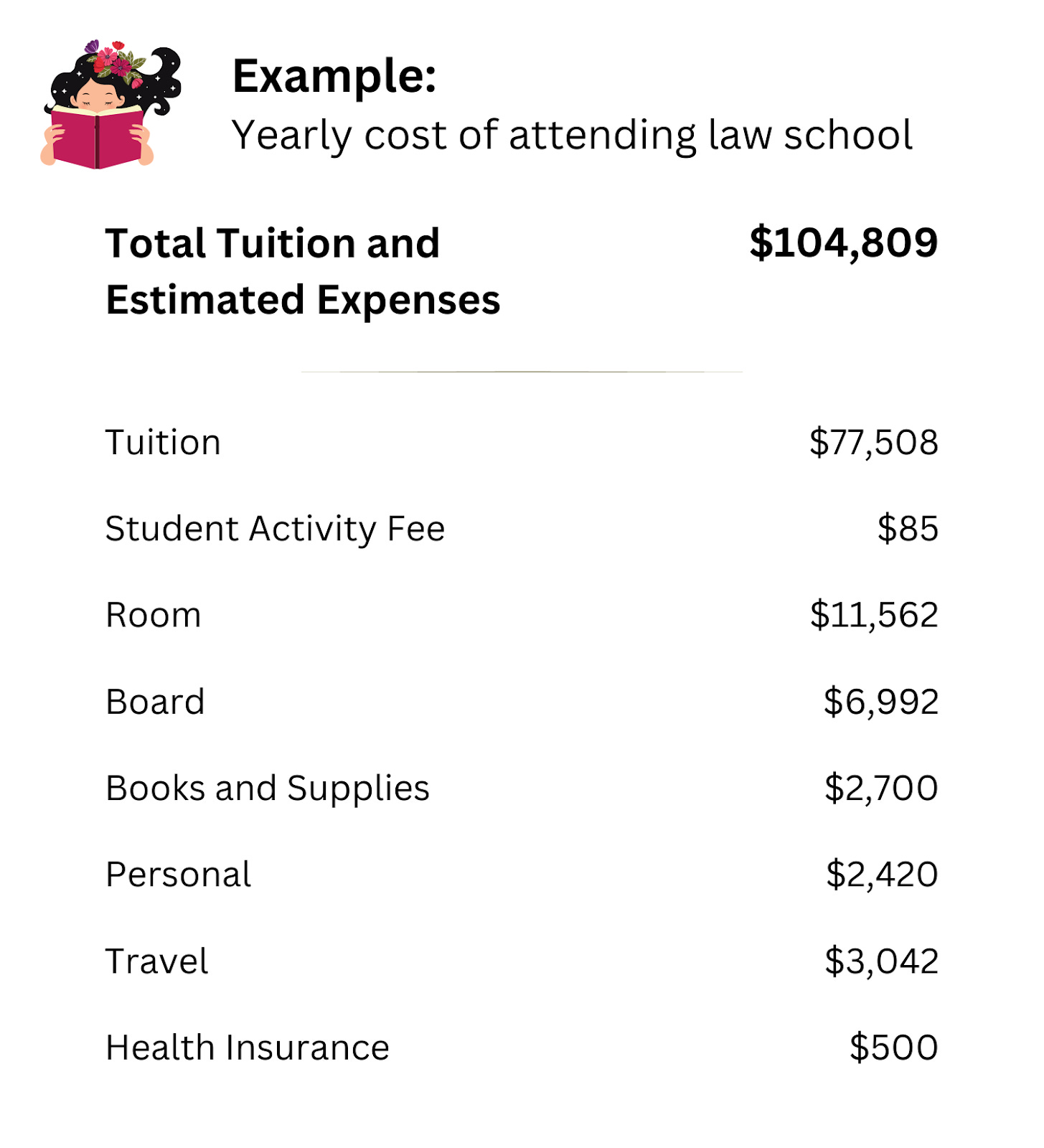

The sticker price, which factors in tuition, room and board, healthcare, and some personal spending, is $100,000+ per year. But all schools practice tuition discounting: they dole out merit scholarships like candy in order to attract students.

Take advantage of tuition discounting! Once you’re admitted, meet with each school’s financial aid officer to negotiate your need-based and merit-based aid. I received $30,000 a year in merit aid from NYU—negotiated up from $25,000—and $45,000 a year in merit aid from Cornell. I cover negotiating merit aid in this post.

A daily fee for your loans

U.S. citizens and permanent residents typically take loans from the federal government — what this post is concerned with.

Your original loan is called your capital. It accrues interest. Interest is like a rental fee for taking out the loan. For loans borrowed in 2023, that interest rate was about 8%.

For a $160,000 capital, your interest grows by about $35 a day. That’s like eating an expensive steak dinner every night 🥩. It adds up to $12,800 a year.

How do you pay off federal loans?

Your payments are always applied to your interest first

Your payments are applied to your interest first, not to the capital.

If your monthly payments are greater than the monthly interest, then you chip into your original loan. Below is an example of what I’m saying.

starting with a loan of $150,000

at 8% interest rate, which adds $1,000/month

with monthly payments of $1,666.67/month

The monthly payment of $1,667 in September is greater than the interest of $1,000, so $667 goes to paying off the capital of $150,000. This causes the capital to drop from $150,000 to $149,334 in October. See how interest then decreases to $996 because capital (original loan amount) decreases? And so on.

If you want to pay off your loans quickly, you want to make larger payments upfront to prevent that interest from piling up.

There are different repayment plans

The federal government expects loan repayment to begin six months after graduation. There are at least six different repayment plans as of 2023.

The 10-year Standard Repayment Plan divides your loans into 120 equal payments. On the other hand, an income-based plan requires you to pay 10% to 20% of your discretionary income1 for 20 to 25 years or until your debt is paid off.

Typically, you choose the 20-year income-based plan when you can’t afford the 10-year standard plan. You’re a do-gooder union-side lawyer living in a closet in Brooklyn with three roommates on $70,000 a year, staring up into the high-rise windows to live vicariously through the trust fund babies and hedge fund managers as you walk to work… (see NYC window economy); there’s no way you’re paying $16,000/year on your $160,000 loan.

So instead of the 10-year plan, you choose an income-based repayment plan that requires paying only 10% of your income — $7,000/year.

So you may never finish paying off your loans

If you’re on that income-based plan paying $7,000 per year, you’re not paying enough to cover your accrued interest. (Recall that for the person with $160,000 in debt, interest grows by $12,800 a year).

This means that by the end of the repayment program, 20 to 25 years later, you still have loans you haven’t paid off. Any remaining loans at the end of your repayment period are forgiven but taxed as income (potentially leading to a ‘tax bomb’).

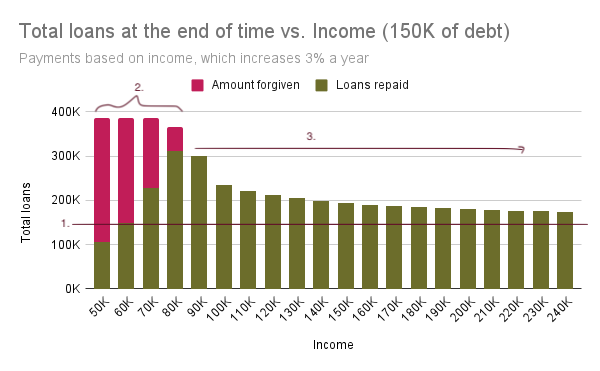

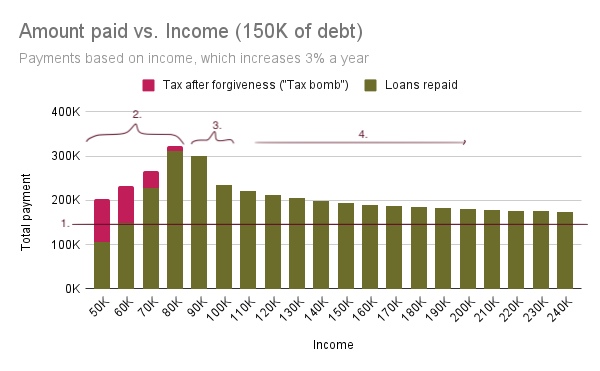

At what income is it impossible to pay off your loans? How much of a tax bomb will you face if you’re left with unpaid loans? The following charts illustrate your total loan burden after 20 years if you took $150,000 in loans, based on different starting salaries.2

Graph 1: Your total debt

In this first graph, total debt is broken into amount paid and amount left over.

Your total debt at the end of time is always greater than $150,000 because the loan accumulates interest (duh!).

At incomes less than $90,000, you don’t have extra cash and are on a 10% income-based plan. Your monthly payments don’t exceed the accruing interest and you never chip into the capital. The debt really takes off, almost reaching $400,000.

Those with an income of more than $100,000/year were able to pay off all their debt because their monthly payments exceeded the accruing interest and chipped into the capital.

Graph 2: The actual amount you pay over a lifetime

In this second graph, you see total paid over time. It is broken up into loan payments and taxed forgiveness.

Everyone pays more than $150,000 because the loan accumulates interest (duh!).

As you can see, low-income earners get hit with that tax bomb. Imagine paying a tax of $100,000 in year 2050. Don’t leave loans unpaid.

Instead, take on less debt, plan to pay off your loans more aggressively, or use a public service loan forgiveness program (PSLF). (PSLF forgives your loans after 10 years with no tax; I’ll cover it in a later post.)

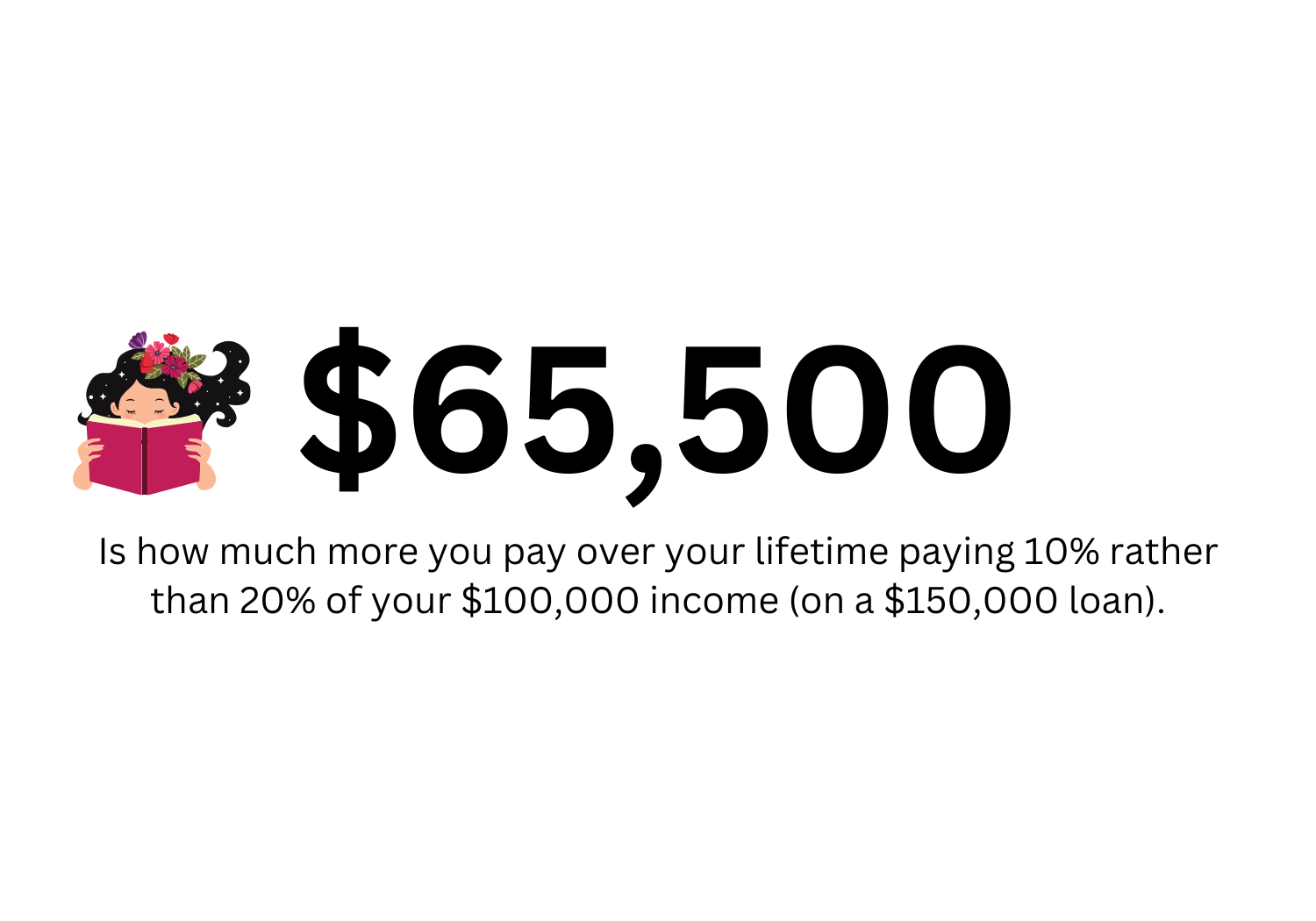

This is important: The person making $90,000 a year paying 10% pays much more over time than someone making $100,000 a year paying 20%. This is because the less you pay, the longer it takes to chip away at your capital and interest racks up.

On the other hand, if you make larger payments, your original loan goes down earlier and interest doesn’t accrue as quickly.

Not pictured: At higher incomes, you’re even paying off your total debt before 20 years is up.

Questions we’ll answer in the next post

Should I always choose the less expensive school?

From a purely financial perspective, it depends on what salary you plan to make.

What income do you realistically make coming out of law school?

It depends on what school you go to, what lifestyle you are willing to live, where you live, and more. I will share a graph of nationwide starting salaries.

What happens if I am planning to be that union-side lawyer making a low salary? Am I doomed?

Enter the Public Service Loan Forgiveness program and have your loans forgiven tax-free after 10 years. Your school may even make your loan payments on your behalf!

Discretionary income is the money you have left after paying for basic needs like housing.

These graphs assume the following:

starting with loans of $150,000 in year one

note I rounded down from $160,000 to $150,000

where 8% simple interest is accrued and never capitalized

When interest is capitalized, it is treated as part of the original loan amount (called ‘capital’). There are limited cases in which interest is capitalized.

you pay 10% up to a salary of $100,000; and 20% above

your monthly payment is calculated from your discretionary income

I assume salary equals AGI, even though AGI may exclude some pre-tax saving like contributing to your 401K.

we assume a steady salary growth of 3% a year (realistic if you stay in the same job or similar ones over time)

you are single with no dependents (for simplicity’s sake)

where any remaining loans at the end of 20 years are forgiven and taxed according to the IRS income brackets

Disclaimer: The analysis below does not account for more complex factors the federal government uses to calculate monthly payments, like your number of dependents, alternate sources of income, state of residence, tax filing status if married, and spouse income and loans (in certain cases). I’ve tried to simplify and illustrate the worst case scenario.

Paying for law school loans sounds a lot like paying off the mortgage on a house. I didn’t expect that!